GoSeigen wrote:CommissarJones wrote:And the move goes on: sterling-priced bullion has topped £1,235/ounce today, after breaking above £1,200/oz at the start of the week. Up 6% in August already. (All according to investing.com.)

If you don't mind my saying so: there are plenty of web sites that publish gold spot prices. Posting just prices of investments is considered bad form on these forums. Very happy to see discussion about the merits of gold as an asset though...

GS

OK GS, I'll bite. Simply because of lockdown boredom.

Harry Markowitz (Nobel prize winner) said, "I visualised my grief if the stock market went way up and I wasn't in it – or it went way down and I was completely in it. So I split my contributions 50/50 between stocks and bonds."

US data, for the Dow/gold ratio, how many ounces of gold to buy the Dow

If instead of stock and bonds, you 50/50 stock and gold, that's a form of neutral stock position, neutral currency position (gold is a form of global currency).

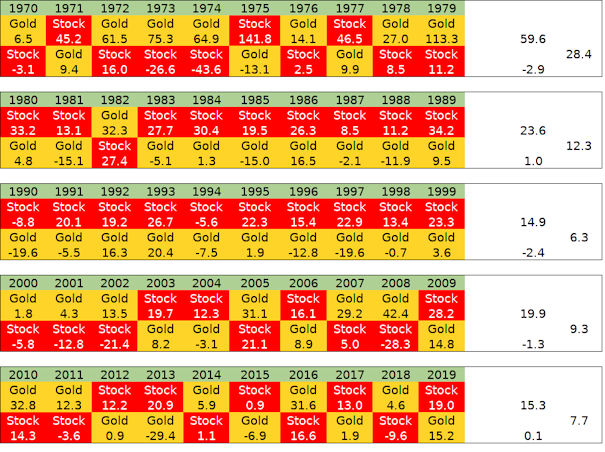

Callan Periodic Table for UK FT All Share total return, gold (£ percentage gains/losses).

To the right I've averaged each decades yearly best and worst assets, and then averaged those two values. Which is indicative that on average the years best asset often spikes up a reasonable amount, whilst the years worst asset doesn't lose much, if at all.

Note also the 1990's where stocks were repeatedly the best asset and gold was the yearly bad asset. Gold ended the 1980’s with a last business day 10am price fix on 29th December 1989 of £249.84 per ounce, and ended the 1990’s at a 30th December 1999 10am price fix of £171.26. Over that decade the nominal price of gold declined -31.5% however the yearly rebalanced accumulation portfolio ended the decade with 2.54 times more ounces of gold in your safe.

Over some prolonged periods you might be cost averaging up the ounces of gold being held, over other periods you might be reducing gold to cost average up the number of stock shares you hold. With often one asset (yearly best) popping to the upside by a 15%, 20% .. or more on a yearly average amount whilst the other (yearly worst) asset around breaks even, which in combination yields a reasonable overall positively biased reward.

Gold's 'dividend' comes out of trading it, leave it as a door stop lump of metal and its a questionable 'investment'. Having some gains arise out of price appreciation, dividends and volatility capture, across asset diversification and currency diversification is a reasonable overall portfolio. Wouldn't want to be all-in gold nor all-in stock, 50/50 middle road is fine.

https://tinyurl.com/y7cm5b7t50/50 stock/gold might be considered as a form of barbell of two extremes, with a central bullet type combined point. I box it into a 'unhedged global bond' type category

https://tinyurl.com/y77we59j More volatile than a bond bullet, but where the volatility in part enables 'trading' (rebalancing) benefits.

Harry Browne took that a stage further and he blended that unhedged global bond bullet with a domestic short dated/long dated treasury barbell (25% in each of stocks, gold, short dated treasury, long dated treasury) that for a US investor from 1972 to the end of March 2020 has yielded nearly a 5% annualised real reward

https://tinyurl.com/y9vy83nz (I used a 10 year bullet in that as it has longer history). Hover your mouse over the (i) symbol next to the CAGR figure in the Portfolio Returns section to see the inflation adjusted value pop-up.

History is weird however. I have data back from 1896 and up to 1931 when the BoE broke away form the gold standard it was more sensible to hold US stock and UK T-Bills/bonds as gold and money were the same (convertible) so it made more sense to have 'gold' earning interest (UK T-Bills) and to hold US stock for £/$ combined 50/50 exposure. After the break off the gold standard it was also more appropriate to hold UK stock and free-floating silver rather than US$ pegged gold. Only after President Nixon broke the US$ away from gold in 1968 as a means to help pay down the cost of the Vietnam war was is appropriate to hold UK stocks and gold. Keeping things at 50% stock, along with 50/50 domestic £ and foreign currency (of which gold is a global currency) kept things neutral. Plug that all into 1896 onwards data and for every 50 year period the worst case PWR (perpetual withdrawal rate) was 4% and the average case was 7% i.e. real gain/withdrawal amounts that left the original inflation adjusted start date value still intact at the end of 50 years. And where that worst case 50 year period was within a total period containing some pretty wild political/social/global extremes. That's just for just the 50/50 portfolio, not the Harry Browne version i.e. as of more recent (since 1968) FT All Share/gold 50/50 yearly rebalanced.

The primary risks are regret - seeing other stock heavy portfolios relatively pull ahead at times inducing you to switch your asset allocation, likely at a bad time. Over other periods you'll be pleased, such as 2008 and recent were pretty much non-events. The above Callan for instance indicates that both 2008 and 2009 were up years. The gold gains in 2008 more than offset the stock declines in 2008. Similarly year to date 2020 and gold is up over +40%, more than offsetting any declines in year to date share price declines.